Improving and maintaining a good credit score isn’t just a financial goal—it’s necessary for anyone planning a significant purchase, like buying a home or a car. Yet, many of us don’t fully understand the factors that impact credit scores or how to improve them effectively. That’s where Jon Liesener, a knowledgeable private banker with deep experience in guiding clients through credit challenges, steps in. He has helped countless individuals build healthier credit profiles, making their financial goals far more achievable.

Whether you’re gearing up for the holiday season, when managing credit cards becomes trickier, or planning for that dream home, this post will help you understand what you need to know about credit scores.

What Are Credit Scores?

Your credit score is a numerical indicator of your creditworthiness, usually between 300 and 850. It provides lenders with insights into how reliably you manage your financial responsibilities. A higher score signals lower risk, which can translate to better loan terms.

Credit scores are calculated using various models, with FICO and Vantage being the most common. Here’s a quick breakdown:

- FICO Score: Used by most lenders, FICO considers factors such as your record of timely payments, the percentage of credit used, and the duration of your credit history.

- Vantage Score: Similar factors are considered here, but the weight may differ slightly, leading to variations in your scores between systems.

💡 Tip: Always review which model your lender uses. It could explain why your free app’s estimate might look different from your lender’s results.

Differences Between FICO and Vantage Scores

Understanding FICO vs. Vantage scores is crucial since a single lender might prioritize one over the other. Key differences include:

- Both use a 300-850 range, but calculations differ slightly.

- FICO heavily weighs payment history and credit utilization.

- Vantage gives more immediate value to recent credit behavior.

- The scores on apps may differ from those seen by lenders. This discrepancy occurs because consumer-facing platforms might use educational versions of these scores instead of lenders’ specific versions.

Knowing which score to focus on can better prepare you for major financial decisions.

Managing Credit Utilization

Credit utilization refers to the percentage of available credit that you are using. It’s a driving force behind your credit score of approximately 30%. The lower your utilization, the better.

Best Practices for Managing Credit Utilization:

- Aim to maintain your credit card balances below 30% of your available credit. For example, if your credit card has a $5,000 limit, aim to keep your balance below $1,500.

- Need extra help managing holiday spending? Create a budget to avoid unnecessary purchases or carrying over balances to the new year.

- Pay balances off in full when possible—this eliminates interest charges and can improve your score.

Proactively managing credit card utilization is one of the simplest ways to boost your score.

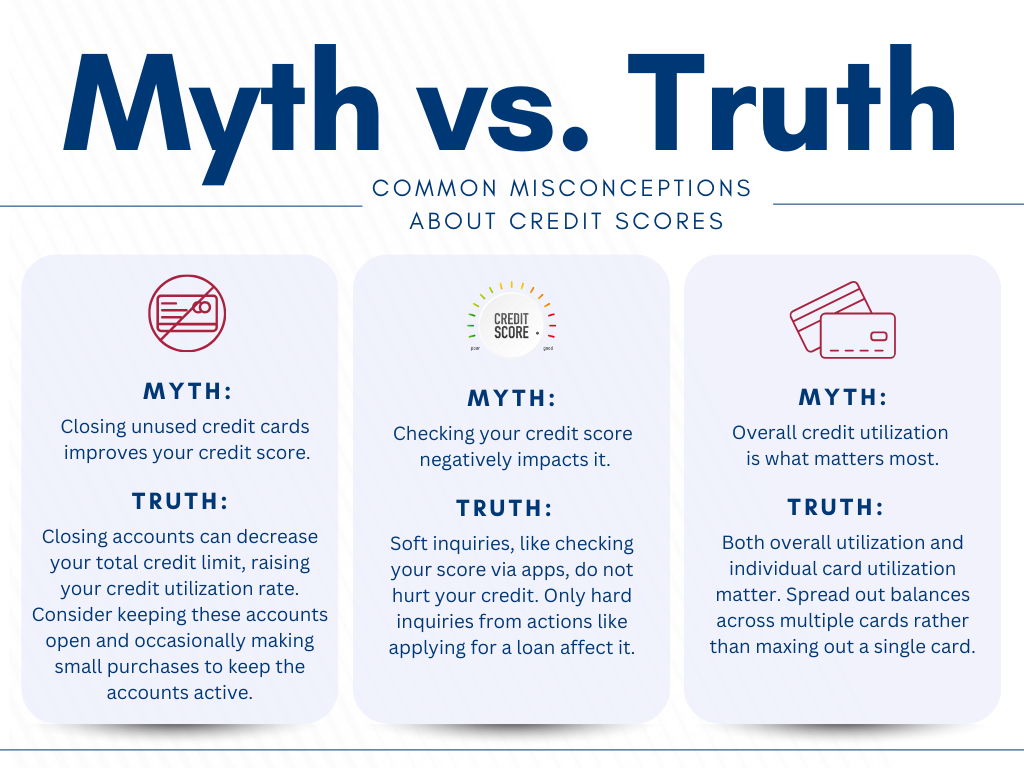

Common Misconceptions About Credit Scores

Credit scores are often misunderstood. Here are a few myths and the truths behind them:

Understanding these nuances can help you manage your credit cards more strategically.

Tips for Improving Your Credit Score

If your credit score needs work, take these actionable steps to turn things around.

Preparing for Big Purchases

Planning for a home or vehicle purchase? Here’s why your credit score matters—and how to prepare for these significant financial milestones:

- Monitor Your Score Regularly: Use tools that provide up-to-date credit scores and reports. Catching issues early prevents unpleasant surprises when lenders pull your credit.

- Save for a Larger Down Payment: While improving your credit score helps, higher down payments can reduce loan requirements and possibly secure better interest rates.

- Talk to a Credit Coach: Credit experts at Heritage Bank can analyze your credit profile, helping you fix issues and strategically position yourself for approval on a big purchase.

Final Thoughts

Improving your credit score involves both knowledge and action. By understanding your FICO and Vantage scores, managing your credit utilization, and avoiding common misconceptions, you’re already on the path to financial success.

Struggling with credit challenges or unsure where to start? Expert help is just a call away. Contact Heritage Bank today for personalized advice and guidance.

Note: This guide is provided for informational purposes only and is not intended as legal or financial advice.

Helping People Succeed Financially. We see every customer as an individual and treat our customers’ businesses as our own. Our dedicated, experienced staff is there for our customers on every step of their journey.