Millions of federal student loan borrowers are facing a harsh reality this summer: wage garnishment could hit their paychecks within months. As of April 2025, 31% of borrowers are 90 days past due on their payments. It is important to understand how delinquency can lead to default and wage garnishment.

If you’re having trouble with student loan payments, this guide can help you take control before it’s too late. Defaulting has consequences that go beyond missed payments. It can hurt your credit score and future borrowing ability. This can affect your financial stability for many years.

The good news? There are proven strategies and federal programs designed to help borrowers avoid default and protect their financial future. Let us explore what you need to know to safeguard your paycheck and get back on track.

Understanding Your Risk of Student Loan Default

Recognizing the warning signs early can make the difference between financial recovery and years of credit damage. Many borrowers unknowingly put themselves at risk through minor oversights.

Common Signs You’re at Risk

The path to default often begins with simple communication breakdowns. If you are ignoring emails or letters from your loan servicer, you are already in dangerous territory. Many borrowers assume they are still in deferment or forbearance without verifying their status, which can lead to unexpected delinquencies.

Another significant risk factor is outdated contact information with your servicer. When borrowers move or change their phone numbers, they often forget to update their records. This can lead to missing important notices about payment due dates, changes in servicers, or available help programs.

It’s also important to know who your current servicer is, as federal loans are frequently transferred between companies. If you don’t know who manages your loans, go to the Federal Student Aid website at StudentAid.gov. There, you can find your loan information and the contact details for your current servicer.

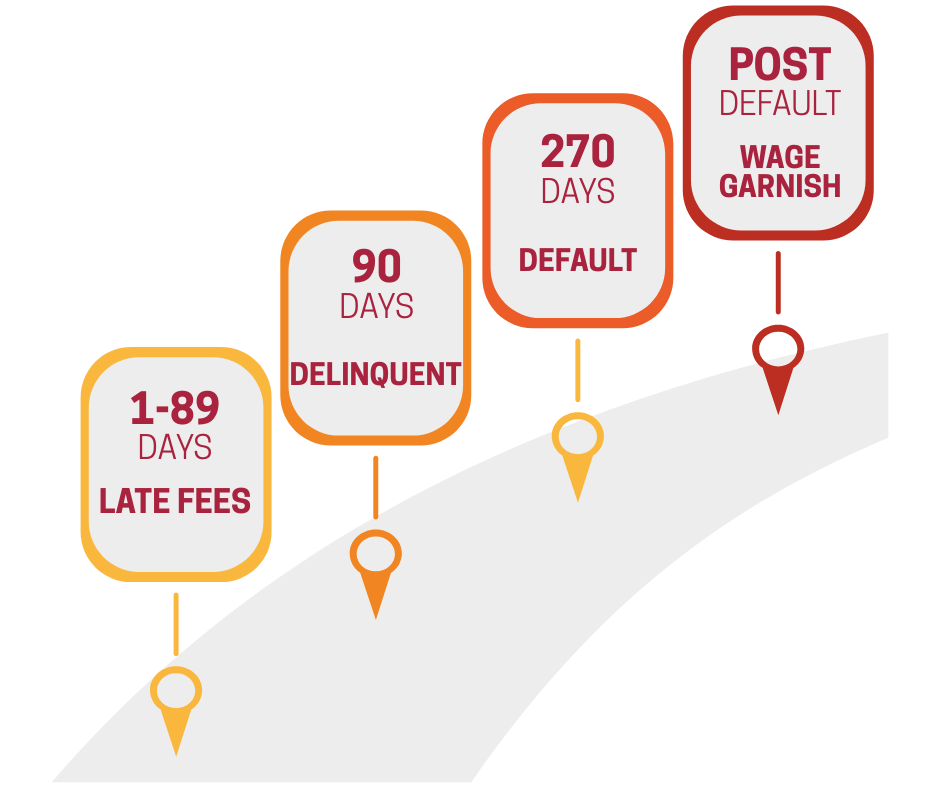

The Timeline That Matters

Understanding the timeline from missed payment to wage garnishment is crucial for taking timely action. Here is what happens:

- Days 1-89: Late payments with potential late fees

- Day 90: Serious delinquency begins, credit reporting starts

- Day 270: Loan enters default status

- Post-default: Wage garnishment proceedings can begin

Once you reach 270 days, the federal government can take up to 15% of your disposable income. They can also withhold your tax refunds and government benefits.

The Reality of Student Loan Wage Garnishment

Many borrowers operate under dangerous misconceptions about the consequences of federal student loans. Unlike other forms of debt, federal student loans carry unique collection powers that borrowers often underestimate.

Debunking Common Misconceptions

One of the most harmful myths is that federal student loans will not result in wage garnishment. The Department of Education stopped collection actions during the pandemic. They followed different rules during this time. However, they started active collection efforts again in May 2025.

Federal student loans also cannot be discharged in bankruptcy like other consumer debts. This means ignoring them will not make them disappear; they’ll continue to grow with interest and penalties while damaging your credit.

Another misconception is that borrowers have unlimited time to figure things out. Once you are 90 days past due, you hurt your credit score. Your options also become more limited.

Immediate Steps if You’re Facing Default

If you’ve already missed multiple payments or received a default notice, swift action is essential. The longer you wait, the fewer options you will have and the more severe the consequences become.

Contact Your Servicer Immediately

Your first call should be to your federal loan servicers. Be honest about your financial situation and ask about available options. Servicers have various tools to help struggling borrowers, including temporary payment reductions, income-driven repayment plans, and forbearance options.

Don’t let pride or fear prevent you from making this call. Servicers would rather work with you to create a manageable payment plan than pursue collection actions.

Explore Income-Driven Repayment Plans

Income-driven repayment plans can significantly reduce your monthly payments based on your income and family size. These federal programs include:

- Income-Based Repayment (IBR)

- Pay As You Earn (PAYE)

- Revised Pay As You Earn (REPAYE)

- Income-Contingent Repayment (ICR)

Some borrowers see their payments reduced to as low as $0 per month, depending on their income level. Even a $0 payment counts as an on-time payment for credit reporting purposes.

Federal Programs to Avoid Garnishment

The federal government offers several programs specifically designed to help borrowers escape default and avoid wage garnishment. Understanding these options can be the key to financial recovery.

Default Resolution Group

If your loan is already in default, it gets transferred to the Default Resolution Group. This group specializes in helping borrowers get their loans out of default through rehabilitation or consolidation programs.

You can reach out to the Default Resolution Group. They will help you make a repayment plan that fits your finances.

Loan Rehabilitation vs. Consolidation

Both rehabilitation and consolidation can remove your loan from default status, but they work differently:

Loan Rehabilitation:

- Requires making nine consecutive, on-time payments

- Payment amount based on your income and expenses

- Removes the default notation from your credit report

- Returns loan to regular servicing

- Can only be used once per loan

Direct Consolidation:

- Combines multiple loans into one new loan

- Requires making three consecutive, on-time payments or agreeing to income-driven repayment

- Default status removed, but delinquency history remains on credit report

- Can be used multiple times

- May result in higher interest rate

The rehabilitation option typically provides better credit score recovery since it completely removes the default from your credit history.

Strategies for Student Loan Repayment Plans

Creating a sustainable budget that prioritizes your student loans is essential for long-term financial stability. Many borrowers find they have more flexibility than they initially realized.

Reassess Your Spending Priorities

TransUnion research reveals that 34% of borrowers who are behind on student loans are paying at least $1,000 more than required on their other debts each month. This suggests that many people have the cash flow to cover their student loans; they need to reallocate their payments.

Start by listing all your monthly expenses and debt payments. Look for areas where you are paying more than the minimum requirement, such as:

- Extra credit card payments

- Additional car loan payments

- Discretionary spending on subscriptions, dining out, or entertainment

Priority Payment Hierarchy

When funds are tight, prioritize payments in this order:

- Housing costs (rent/mortgage, utilities)

- Essential transportation (car payment if needed for work)

- Minimum payments on all debt (to avoid delinquencies)

- Student loans (to prevent default)

- Extra payments on highest-interest debt

- Discretionary spending

Helpful Budgeting Tools

Several free tools can help you create and maintain a realistic budget:

- 50/30/20 Rule: Allocate 50% to needs, 30% to wants, 20% to savings and debt repayment

- Your bank’s budgeting tools: Many financial institutions offer free budgeting resources

The key is finding a system you will use consistently. Budgeting for student loan repayment can pay off if you can maintain a realistic plan.

Protecting Your Credit Score

Your credit score impacts everything from mortgage rates to job opportunities. Understanding how student loan delinquencies affect your credit can motivate prompt action and help you make informed decisions.

Impact of Student Loan Delinquencies

Student loan delinquencies can hurt your credit score. This effect is strongest for borrowers who begin with higher scores. Even after you pay off your loan, the late payment note stays on your credit report for up to seven years. This can still affect your ability to borrow money and the interest rates you receive.

Strategies to Minimize Credit Damage

Stay current on all your other obligations while addressing your student loan issues. Don’t rob Peter to pay Paul by missing credit card or auto loan payments to catch up on student loans. This approach creates multiple delinquencies and compounds your credit problems.

Rebuilding Financial Stability After Default

Recovery from student loan default is possible, but it requires patience, discipline, and a strategic approach. Focus on sustainable progress rather than quick fixes.

Focus on Getting Current

The most key step is bringing your loans back to good standing through rehabilitation or consolidation. This process typically takes 9 to 12 months for rehabilitation. However, it is worth the effort. It helps restore your access to financial aid and improves your credit profile.

Keep making all your other debt payments on time. This will help you avoid more negative marks on your credit report. Every on-time payment helps rebuild your creditworthiness.

Avoid New Debt

While rebuilding, resist the temptation to take on additional debt unless necessary. This includes store credit cards, personal loans, or financing offers. Focus your financial energy on resolving existing obligations and building emergency savings.

If you need to take on new debt, like a car loan after an accident, be careful. Choose wisely when and where you apply for credit.

Proactive Steps to Avoid Future Delinquency

Prevention is always better than cure when it comes to student loan default. These proactive strategies can help you stay on track and avoid future problems.

Stay Informed and Engaged

Never ignore communications from your loan servicer, even if the news is not what you want to hear. Open and read all mail and emails promptly. If you don’t understand something, please call and ask for clarification.

Keep your contact information up to date with your loan servicer. This includes your address, phone number, and email address. Set up automatic notifications if available to ensure you never miss important updates.

Communicate Early and Often

If you anticipate difficulty making payments due to job loss, illness, or other financial hardship, contact your loan servicer immediately. Do not wait until you’ve already missed payments. Early communication opens up more options and demonstrates good faith on your part.

Most loan servicers can offer temporary help through deferment, forbearance, or modified payment plans. You should contact them before the problems worsen.

Taking Control of Your Financial Future

Student loan default and wage garnishment are not inevitable, even if you are already behind on payments. The key is to take action before your options become limited, and the consequences are more severe.

Remember that federal student loans offer more flexible repayment options than most other types of debt. Income-driven repayment plans, rehabilitation programs, and consolidation options provide multiple pathways back to good standing.

Your current financial struggles don’t define your future. Many borrowers successfully navigate through default and go on to achieve their financial goals. Act quickly. The sooner you do, the sooner you can overcome this challenge. Then, you can focus on building the financial stability you deserve.

Do not wait for garnishment to be deducted from your paycheck. Contact your loan servicer today or explore your options with the Default Resolution Group. You can also visit StudentAid.gov to access your loan information and find additional resources. Taking a few proactive steps now can protect your financial future and help you get back on the path to success.